As part of my advocacy work, I get to hear a lot about what is challenging businesses daily. One of the most common complaints is that people are rejected from loans in order to build their business. So let’s talk about loans, how to get your credit up, and what to do if you can’t wait that long to get the bank to say yes.

What’s your relationship with money?

The first thing we need to address is your own relationship with money. If you don’t have great credit and a ton of money in the bank (hey, you’re reading this article, so that’s probably you), then it’s time to examine what money is and what it can do for you?

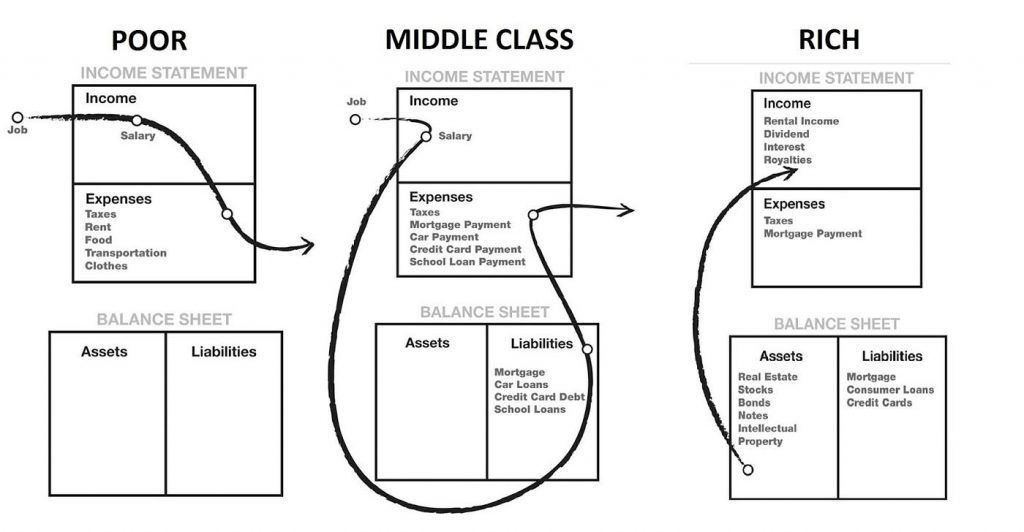

Money is just money – but as Robert Kiyosaki has pointed out in his book Rich Dad, Poor Dad, money can make you a slave or set you free.

While I want you to go down that rabbit hole if you haven’t, I’ve linked enough information for you to get where you need to go to take you to the next step:

- Cash is not freedom. People who do not understand how money works in a capitalist society will stock cash away in their mattresses and brag about being debt free and not having credit cards, but if you want to grow and you think this is the way, you’re missing out on two thins.

- Money in the bank makes YOU money. You put that money in a mattress and it loses money every year due to depreciation. Put it in a High Yield Savings account (I’d like to one but you need to do research) and it will make money. Just sitting there. The banks are insured, typically, up to $250,000 so even if the bank fails, that money is safe. Got more than that? Open up another account.

- Debt makes you money, too. This is the biggest one to get into your head, and it’s what Robert Kiyosaki got so right. Don’t believe me? Play his game, Cashflow. Find out how if you take out a loan on something and pay interest on it, but you can MAKE more money holding the asset, even with the loan, that’s the way to freedom.

- Debt is freedom. If you stop thinking about how much you owe, and start thinking about how much access you have to what you need, the world is your oyster. Yes, you’ll be paying off loans and paying interest, but someone’s giving you money to grow a thing, right now. Not in years when you can squirrel it away.

Okay, so can we agree that debt is good? Great, let’s move on.

Getting started

You don’t need a ton of money to get started unless you’re thinking really big. Most of us aren’t. If you ARE thinking big, then business school (and that debt load) or putting yourself into employment situations that pay you to learn what you need to are the right ways to go. You can stop reading and go out and do that now. Both will take a few years, and if you start small, you might be there anyway, though.

What do you need to do to get started TODAY?

- Invest a little. Don’t lose your house over it. Start something small, get your product launched that you know someone wants (plenty of books on that) and then spend all your time learning how to get it into people’s hands. Read $100 Start Up to get inspired (surprise, I’m in it, too).

- Build your reputation. Once people like it, you’ll end up with a few people that become your champions. These folks will sell your product for you. Help them do that. This is building credit, btw. We’ll get there soon.

Let’s start building credit.

- At some point, you’re going to need more money to make more product you and your champions are selling and this is where it gets weird. Especially if you’ve been squirreling money without taking out a credit card. Take out a credit card. I don’t care if the card has 45% interest, get one. Put your Netflix subscription on there and set autopay to pay it off as soon as the subscription hits. You won’t get interest charged – but you’ll get credit.

- Once you get credit, they want to give you more credit. Be smart. Pay that bill off before it’s due and don’t pay interest. Start checking your credit scores and note that they’ll start offering you better cards – and personal loans. That’s nice. Note it.

- Call in and request more credit or an interest rate drop or both. You’re a good customer, they aren’t coming for you, they want to give you more. It’s a service YOU are providing, so take control. It never hurts to ask. Do it every six months.

- When they start saying yes, it’s time to look for a credit card that gives cash back. Now you’re making money on that card because you’ve built the habit of not paying interest.

Using credit to build your business

Now you’ve built two kinds of credit early in your business journey: personal and capital.

Personal = you’ve got people who like you and what you’re selling it and are selling it for you.

Capital = you have access to money to borrow.

Now you can build your company two ways:

- Investment (or crowdfund loans) because you have friends and family who want to give you money in exchange for perks like dividends or special products just for them

- Credit – so you can buy something and pay interest and still make more money than if you didn’t borrow.

Congratulations! Do that over and over and in a year or two, the banks will give you money. Keep doing it and you’ll out grow your bank and find a new bank who will say yes.

Keep going!